Indicators

Activities, value chain and other business relationships

GRI 2-6

2-6 a) Report the sector(s) in which it is active.

The Banrisul serves the public and private sectors in all economic segments, including civil servants, private sector employees, self-employed professionals and farmers.

2-6 b) Describe its value chain, including:

2-6-b) i) the organization’s activities, products, services, and markets served;

In its commercial portfolio, Banrisul grants lines of credit to various segments, including to small businesses. For the Rio Grande do Sul’s local governments, it offers lines of credit with its own funds to finance capital goods, and on-lending lines of the Brazilian Development Bank (BNDES, in Portuguese) for businesses installation and expansion projects.

Banrisul’s operations serve both the individual and corporate segments and provide commercial, real estate, and rural financing. Banrisul and the group’s companies offer their customers a wide range of financial products and services, including credit cards, securities brokerage, consortium management, payment methods, insurance, private pension plans, capitalization bonds, and intermediation in both variable and fixed income, as well as foreign exchange transactions.

2-6-b) ii) the organization’s supply chain;

Banrisul and its affiliates currently have several types of suppliers: lawyers, consultants, system analysts, vendors of perishable and non-perishable goods, international IT companies, armored truck companies and numerous other service and providers.

2-6-b) iii) the entities downstream from the organization and their activities.

Banrisul acts as a financial agent for customers from industry, agriculture, transport, service, trade and health sectors. Most of them are located in Brazil’s South region.

2-6 c) Report other relevant business relationships.

There are no other relevant business relationships.

2-6 d) Describe significant changes in 2-6-a, 2-6-b, and 2-6-c compared to the previous reporting period.

There were no significant changes.

Activities, value chain and other business relationships

GRI 2-6

Banrisul operates in the public and private sectors. The Bank and its affiliates currently have several types of suppliers: lawyers; consultants; system analysts; sellers of perishable and non-perishable goods; international IT companies; armored truck companies; and numerous other service providers.

The number of direct suppliers, in 2022, is estimated at 1,093. The Bank hires suppliers to provide services and products unrelated to its core activity, i.e., they provide supporting services and products, including security, cleaning, transportation of valuables, acquisition of IT systems, telephone and internet services, acquisition of furniture, building rental, acquisition of sundry items.

Banrisul acts as a financial agent for customers, from industry, agriculture, transport, service, trade and health sectors. Most of them are located in Brazil’s South region.

Activities, value chain and other business relationships

GRI 2-6

2-6 a) Report the sector(s) in which it is active;

We serve the public and private sectors in all economic segments — including civil servants —, private sector employees, self-employed professionals and farmers.

2-6 b) Describe its value chain, including:

2-6 b) i) the organization’s activities, products, services, and markets served;

In our commercial portfolio, we grant credit lines to several segments, including to small businesses. For the Rio Grande do Sul’s local governments, we offer credit lines with our own funds to finance capital goods, and on-lending lines of the Brazilian Development Bank (BNDES, in Portuguese) for businesses’ installation and expansion projects.

Banrisul’s operations cover the individual and corporate segments and offer commercial, real estate and rural financing. Banrisul and the Group’s companies offer customers a broad range of financial products and services, including credit cards, securities brokerage, sales pool group management, means of payment, insurance, private pension plans, savings bonds and intermediation of variable and fixed income and foreign exchange transactions.

2-6 b) ii) the organization’s supply chain;

Our supply chain consists of lawyers, consultants, systems analysts, salespeople, international technology companies, money transportation companies, and other types of service providers.

2-6 b) iii) the entities downstream from the organization and their activities;

We act as a financial agent for our customers, covering the industry, agriculture, transportation, services, commerce, and healthcare sectors.

2-6 c) Report other relevant business relationships;

There are no other relevant business relationships.

2-6 d) Describe significant changes in 2-6-a, 2-6-b, and 2-6-c compared to the previous reporting period.

There have been no significant changes in the value chain or in the supply chain.

Activities, value chain, and other business relationships

GRI 2-6

2-6 a) Report the sector(s) in which it is active.

We operate in the commercial, credit, financing and investment, mortgage, development, leasing, and foreign exchange sectors, serving diverse customer segments, including individuals, businesses, farmers, and public entities.

2-6 b) Describe its value chain, including:

2-6 b) i) the organization’s activities, products, services, and markets served;

We operate in the commercial, credit, financing and investment, mortgage, development, leasing, and foreign exchange sectors, serving diverse customer segments, including individuals, businesses, farmers, and public entities.

Through our subsidiaries and affiliates, we also operate in other important areas, notably securities brokerage, management of consorcios (pre-purchase financing pools), payment methods, insurance, and pension plans.

We also serve as an instrument for implementing the economic and financial policy of the State of Rio Grande do Sul, in alignment with the State Government’s plans and programs.

2-6 b) ii) the organization’s supply chain;

In the course of our operations, we establish business relations with various types of organizations, including service providers, technology vendors, specialized consulting firms, partner financial institutions, and other entities that support the execution of our operations and strategic initiatives. These relationships are formalized contracts and are monitored according to technical, legal, and compliance criteria.

2-6 b) iii) the entities downstream from the organization and their activities.

We serve different customer segments, including individuals, businesses, farmers, and public entities.

2-6 c) Report other relevant business relationships.

Banrisul currently has no joint ventures or corporate alliances, but has significant institutional partnerships such as the Impacta RS Program (SICT, Coalizão pelo Impacto, Regenera RS, and Finep) and partnerships with Badesul, BRDE, and BNDES.

2-6 d) Describe significant changes in 2-6 a), 2-6 b), and 2-6 c) compared to the previous reporting period.

There were no significant changes.

Annual total compensation ratio

GRI 2-21

2-21 a) Report the ratio of the annual total compensation for the organization’s highest-paid individual to the median annual total compensation for all employees (excluding the highest-paid individual).

The ratio between the highest total annual compensation and the average annual compensation of the Company’s other employees was 11.09.

2-21 b) Report the ratio of the percentage increase in annual total compensation for the organization’s highest-paid individual to the median percentage increase in annual total compensation for all employees (excluding the highest-paid individual).

There was a 2.5% decrease in the highest salary between 2024 and 2025. In contrast, among the other employees who worked the entire year, the average salary increased by 4.2%.

2-21 c) Report contextual information necessary to understand the data and how the data has been compiled.

The individual with the highest annual salary at the company is the CEO. For analysis purposes, we calculated the ratio of the CEO’s compensation to the average annual salary of other employees who worked all 12 months of the year, excluding those who joined or left the company during that period. For each individual, both fixed and variable compensation received throughout 2025 were considered.

Annual total compensation ratio

GRI 2-21

The ratio of the annual total compensation for the organization’s highest-paid individual to the median annual total compensation for all employees is 12.0%, while the ratio of the percentage increase in the annual total compensation for the organization’s highest-paid individual to the median percentage increase in the annual total compensation for all employees is 0.8%.

Annual salary increases occur in April (regulatory promotions retroactive to January) and in September (collective bargaining agreement).

For calculation purposes, the CEO, who is not a Bank employee, was considered as the highest-paid individual. The other workers who are not employees were not considered in the calculation. The total compensation (salaries, bonuses, job commission, full performance bonus, annual bonus, overtime, singing bonus, relocation bonus, management, retirement bonus, and retirement incentive) was considered in calculating compensation.

Annual total compensation ratio

GRI 2-21

2-21 a) Report the ratio of the annual total compensation for the organization’s highest-paid individual to the median.

The ratio of the annual total compensation of the organization’s highest paid individual and the average annual total compensation of all other employees (excluding the highest paid) was 10%.

2-21 b) Report the ratio of the percentage increase in annual total compensation for the organization’s highest-paid individual to the median percentage increase in annual total compensation for all employees (excluding the highest-paid individual).

The median remuneration of employees, excluding the highest paid, fell from 2022 to 2023, due to the dismissal of 506 employees through the Voluntary Severance Program, so it was not possible to calculate the proportion of the percentage increase requested in item b.

2-21 c) Report contextual information necessary to understand the data and how the data has been compiled.

The Chief Executive Officer was not included in this calculation, since there was a change to the Board of Executive Officers. The reference was the Deputy Chief Executive Officer, who is not an employee of the Bank. Total compensation included salaries, bonuses, job commission, full-time dedication bonus and length of service bonus, overtime, singing bonus, relocation bonus, executive officer bonus, retirement bonus and incentivized retirement plan.

Annual total compensation ratio

GRI 2-21

2-21 a) Report the ratio of the annual total compensation for the organization’s highest-paid individual to the median annual total compensation for all employees (excluding the highest-paid individual);

In 2024, the ratio between the Company’s highest annual salary and the average annual salary for other employees (excluding the highest-paid individual) was 8.97%.

2-21 b) Report the ratio of the percentage increase in annual total compensation for the organization’s highest-paid individual to the median percentage increase in annual total compensation for all employees (excluding the highest-paid individual);

The highest salary increased by 13.8%, while the average salary for other employees fell by 1.8%, reflecting the dismissal of highly paid employees. The highest salary refers to different positions in 2023 and 2024, due to the later definition of all members of the Executive Board in the report.

2-21 c) Report contextual information necessary to understand the data and how the data has been compiled.

The Company’s CEO was the highest-paid individual in the reporting period, considering fixed and variable fees.

Approach to stakeholder engagement

GRI 2-29

Stakeholder categories with whom Banrisul engages are:

- Employees;

- Shareholders/investors;

- Market analysts;

- Customers;

- Suppliers;

- Government;

- Unions;

- Executive Board;

- Board of Directors;

- Social, Environmental and Climate Responsibility Committee – CRSAC.

The Institution has identified the need to create a stakeholder engagement program to strengthen its relationship with these groups and provide greater business opportunities and chances to listen to them. The goal is that this program enables the Institution to explore relationship channels with several groups.

For preparing its materiality, Banrisul surveyed all its target audiences, creating an opportunity to get to know their interests.

Approach to stakeholder engagement

GRI 2-29

2-29 a) Describe its approach to engaging with stakeholders, including:

2-29 a) i) the categories of stakeholders it engages with, and how they are identified;

- Employees

- Shareholders/investors

- Market analysts

- Customers

- Suppliers

- Government

- Unions

- Board of Executive Officers

- Board of Directors

- Social, Environmental and Climate Responsibility Committee – CRSAC Sustainability Committee

2-29 a) ii) the purpose of the stakeholder engagement;

Banrisul focused its efforts on engaging its stakeholders, especially internal stakeholders and managers. Due to the hiring of new employees and the fact that it was a year marked by changes in the Institution’s management, Banrisul intensified its efforts to connect employees and engage these professionals in the new strategic guidelines.

2-29 a) iii) how the organization seeks to ensure meaningful engagement with stakeholders.

Through the Onboarding Program, the People and Culture Development Unit – Corporate University, responsible for organizing the program, provided newcomers with a unique experience that allowed them to deepen their knowledge of Banrisul’s history, mission, culture, values, practices and goals. The initiative reinforces the Bank’s commitment to the continuous training of its employees, striving for constant improvement.

Approach to stakeholder engagement

GRI 2-29

2-29 a) Describe its approach to engaging with stakeholders, including:

2-29 a) i. the categories of stakeholders it engages with, and how they are identified;

Our key stakeholder groups include employees, shareholders, market analysts, customers, suppliers, government, labor unions, regulatory bodies and senior management.

2-29 a) ii. the purpose of the stakeholder engagement;

We value maintaining ongoing dialogue with stakeholders, aimed at aligning our strategic guidelines with market trends and stakeholder expectations. We are constantly seeking to strengthen these relationships, promoting mutual listening and development opportunities.

2-29 a) iii. how the organization seeks to ensure meaningful engagement with stakeholders. We strive to ensure meaningful engagement through initiatives aimed mainly at integrating new employees, thus reinforcing our corporate culture right from the beginning of their journey.

We strengthened our relationship with external audiences, customers and communities by engaging them in specific events and initiatives, expanding our social presence and the Bank’s role as a development agent in Rio Grande do Sul.

Approach to stakeholder engagement

GRI 2-29

2-29 a) Describe its approach to engaging with stakeholders, including:

2-29 a) i) the categories of stakeholders it engages with, and how they are identified;

Banrisul’s main target audiences include:

- Customers and users of financial services.

- Employees and managers.

- Shareholders and investors.

- Suppliers and business partners.

- Regulatory bodies and government entities.

- Communities and society at large.

- Media and opinion leaders.

2-29 a) ii) the purpose of the stakeholder engagement;

Relationships with stakeholders are essential to our operations and to management practices aligned with the expectations of society and the market. We are in constant dialogue with diverse stakeholders in order to understand their needs, strengthen relationships of trust, and incorporate their inputs into our decision-making processes.

2-29 a) iii) how the organization seeks to ensure meaningful engagement with stakeholders.

This engagement takes place through institutional channels and relationship-building initiatives that help identify perceptions, expectations, and opportunities for improvement. Interaction with stakeholders also contributes to the development of products and services, the strengthening of governance, and the advancement of sustainability initiatives.

Dialogue takes place through diverse means, including customer service channels, institutional meetings, satisfaction surveys (NPS), relationship programs, digital platforms, and events. Communication with the press is handled by the Press Office, which is responsible for institutional positions and communication strategies. For investor relations, we have specific channels, such as “Contact IR” and a dedicated email address, ensuring transparent and prompt response to requests for corporate and financial information.

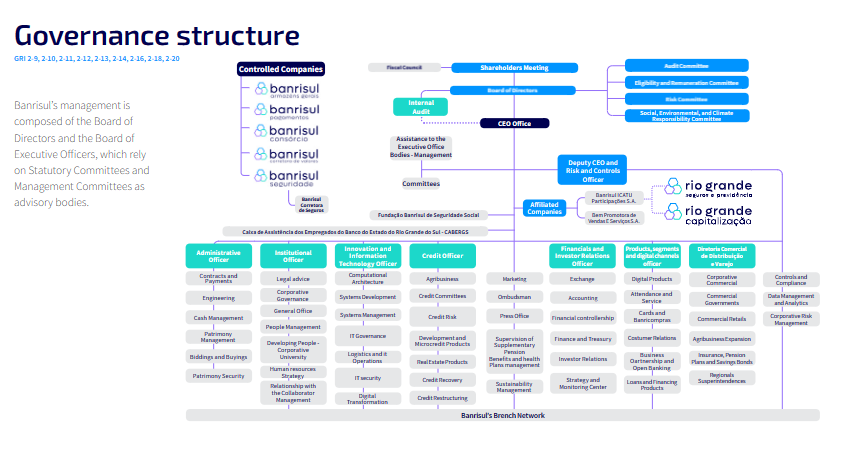

Chair of the highest governance body

GRI 2-11

2-11 a) Report whether the chair of the highest governance body is also a senior executive in the organization;

2-11 b) If the chair is also a senior executive, explain their function within the organization’s management, the reasons for this arrangement, and how conflicts of interest are prevented and mitigated.

The chair of the Board of Directors is not a senior executive at Banrisul.

Chair of the highest governance body

GRI 2-11

The Chair of the Board of Directors is not the Company’s CEO.

Chair of the highest governance body

GRI 2-11

2-11 a) Report whether the chair of the highest governance body is also a senior executive in the organization.

2-11 b) If the chair is also a senior executive, explain their function within the organization’s management, the reasons for this arrangement, and how conflicts of interest are prevented and mitigated.

The Chair of the Board of Directors is not a senior executive at Banrisul.

Chair of the highest governance body

GRI 2-11

2-11 a) Report whether the chair of the highest governance body is also a senior executive in the organization.

The chair of the Board of Directors is not in Banrisul’s CEO.

2-11 b) If the chair is also a senior executive, explain their function within the organization’s management, the reasons for this arrangement, and how conflicts of interest are prevented and mitigated.

The chair of the Board of Directors is not in Banrisul’s CEO.

Collective bargaining agreements

GRI 2-30

2-30 a) Report the percentage of total employees covered by collective bargaining agreements.

100% of employees are covered by collective bargaining agreements.

2-30 b) For employees not covered by collective bargaining agreements, report whether the organization determines their working conditions and terms of employment based on collective bargaining agreements that cover its other employees or based on collective bargaining agreements from other organizations.

All employees are covered by collective bargaining arrangements, in particular the Collective Bargaining Agreement and its amendment.

Collective bargaining agreements

GRI 2-30

2-30 a) Report the percentage of total employees covered by collective bargaining agreements.

2-30 b) For employees not covered by collective bargaining agreements, report whether the organization determines their working conditions and terms of employment based on collective bargaining agreements that cover its other employees or based on collective bargaining agreements from other organizations.

100% of the employees are covered by the collective bargaining agreement.

Collective bargaining agreements

GRI 2-30

2-30 a) Report the percentage of total employees covered by collective bargaining agreements;

100% of employees are covered by collective bargaining agreements.

2-30 b) For employees not covered by collective bargaining agreements, report whether the organization determines their working conditions and terms of employment based on collective bargaining agreements that cover its other employees or based on collective bargaining agreements from other organizations.

100% of employees are covered by collective bargaining agreements.

Collective bargaining agreements

GRI 2-30

100% of employees are covered by collective bargaining agreements.

Collective knowledge of the highest governance body

GRI 2-17

2-17 a) Report measures taken to advance the collective knowledge, skills, and experience of the highest governance body on sustainable development.

Our management participates annually in specialized courses, covering topics such as corporate law, financial markets, internal controls, code of ethics, Anti-Corruption Law and other matters considered relevant to the Company’s activities.

Collective knowledge of the highest governance body

GRI 2-17

2-17 a) Report measures taken to advance the collective knowledge, skills, and experience of the highest governance body on sustainable development.

Every year, Management takes specific courses on topics such as corporate and financial market laws, data disclosure, internal controls, the code of ethics, the Anti-Corruption Law and other subjects related to Banrisul’s activities. In 2023, sustainability and ESG guidelines were included in the lectures, as requested by Management.

Collective knowledge of the highest governance body

GRI 2-17

2-17 a) Report measures taken to advance the collective knowledge, skills, and experience of the highest governance body on sustainable development.

Members of Senior Management regularly participate in training and refresher programs on topics relevant to the management of the Institution, including corporate and financial market legislation, disclosure of corporate information, internal controls, ethics and integrity, as well as aspects related to the Anti-Corruption Law and regulatory standards applicable to the financial system.

Collective knowledge of the highest governance body

GRI 2-17

In compliance with Law 13,303/16, every year, elected Management members attend specific training on corporate and capital market legislation, disclosure of information, internal controls, code of conduct, Law 12,846, of August 1, 2013 (Anti-Corruption Law) and other topics related to the activities of a publicly held company or government-controlled company. In 2022, ESG was included in the list of topics. Additionally, Management members may participate in other courses/events with themes pertinent to their responsibilities in the respective governance bodies, if said theme is interesting for the Company.

Communication of critical concerns

GRI 2-16

Suspicions or evidence of non-compliance with Banrisul’s Code of Ethics and Conduct, policies, standards and institutional regulations in force should be reported through the Whistleblowing Channel, which allows the anonymous reporting of the misconduct, ensuring the right to confidentiality and protection against retaliation. The internal and external channels are available, respectively, on the Corporate Intranet and on Banrisul’s website (www.banrisul.com.br) and are intended for receiving misconduct reposts and complaints from employees and other stakeholders. The Control and Compliance Department is the independent area responsible for managing this channel.

Every six months the Board of Directors reviews a report on Banrisul’s Whistleblowing Channel. In compliance with article 3, paragraph 2, of CMN Resolution 4,859/2020, the Control and Compliance Department prepares a report with the following minimum information:

I – the number of reports received;

II – the nature of the reports;

III – the departments responsible for handling the situation;

IV – the average response time; and

V – the measures adopted by the Institution.

Communication of critical concerns

GRI 2-16

2-16 a) Describe whether and how critical concerns are communicated to the highest governance body.

At its ordinary or extraordinary meetings, the Board of Directors receives and resolves on the concerns reported by the Executive Board and the Statutory Audit, Eligibility and Remuneration, Risk and Social, Environmental and Climate Responsibility Committees. In addition to these, the crucial concerns received through the Whistleblowing Channel are communicated to the Board of Directors by means of reports which must contain, at the very least, the number and nature of the communications received, the areas responsible for dealing with the situation, the average time for treatment and the measures adopted by the Institution. If it is proven that employees engaged in wrongdoing, the complaints are brought to the attention of the Ethics Committee.

2-16 b) Report the total number and the nature of critical concerns that were communicated to the highest governance body during the reporting period.

The number and nature of critical concerns are deemed confidential by Banrisul.

Communication of critical concerns

GRI 2-16

2-16 a) Describe whether and how critical concerns are communicated to the highest governance body;

The Whistleblowing Channel, available on the Bank’s website and intranet, allows the reporting of suspected or actual violations to the Code of Ethics, which are investigated internally. Periodic reports are submitted to senior management.

2-16 b) Report the total number and the nature of critical concerns that were communicated to the highest governance body during the reporting period.

Information not disclosed due to its confidentiality.

Communication of critical concerns

GRI 2-16

2-16 a) Describe whether and how critical concerns are communicated to the highest governance body.

We have a Whistleblower Channel to receive reports from employees, management, customers, suppliers, and other stakeholders regarding irregularities, such as fraud, corruption, harassment, or non-compliance with the Code of Ethics and Conduct.

2-16 b) Report the total number and the nature of critical concerns that were communicated to the highest governance body during the reporting period.

Banrisul considers the number and nature of these critical concerns to be confidential, since the data is restricted and generally sensitive to the institution.

Company information

GRI 2-1

Banco do Estado do Rio Grande do Sul (Banrisul) is a government-controlled corporation. Banrisul’s General Management, its administrative headquarters, is located in the city of Porto Alegre, Rio Grande do Sul state.

Compliance with laws and regulations

GRI 2-27

2-27 a) Report the total number of significant instances of non-compliance with laws and regulations during the reporting period, and a breakdown of this total by:

2-27 a) i) instances for which fines were incurred;

2-27 a) ii) instances for which non-monetary sanctions were incurred.

In 2023 there were no significant incidents of non-compliance with laws and regulations¹

¹For 2023, in an effort to improve information management, the scope of the indicator was limited to fines and sanctions imposed on the institution in relation to its direct conduct on these issues. In this period, non-compliance incidents that cause social, environmental or climate damage are considered. For this reason, figures published for previous years have been adjusted in this report. This has led to a reduction in the number of cases presented.

2-27 b) Report the total number and the monetary value of fines for instances of noncompliance with laws and regulations that were paid during the reporting period, and a breakdown of this total by:

2-27 b) i) fines for instances of non-compliance with laws and regulations that occurred in the current reporting period;

2-27 b) ii) fines for instances of non-compliance with laws and regulations that occurred in previous reporting periods.

Cases of non-compliance with laws and regulations¹ |

|||

|---|---|---|---|

2023 |

During previous reporting periods (2017 to 2022) |

||

Number of cases |

Monetary value (R$) |

Number of cases |

Monetary value (R$) |

1 |

R$8,000 |

3 |

R$49,000 |

¹All loss events involving administrative and court proceedings, administrative fines and damage to physical assets were considered as fines, such as events associated with bad weather and damage to physical assets (climate scope), data processing and over-indebtedness (social scope).

2-27 c) Describe the significant instances of non-compliance.

Significant cases of non-compliance consist of the total number of operational risk events with a social, environmental and climate scope, comprising fines, notices, damage to physical assets, administrative and legal proceedings (civil and labor) against the Banrisul Group.

2-27 d) Describe how it has determined significant instances of non-compliance.

The instances of social, environmental and climate non-compliance are identified based on Section VIII — Management of social, environmental and climate risks (articles 38-A, 38-B, 38-C) of Resolution 4,557/17 of the National Monetary Council. The articles mentioned above exemplify social, environmental and climate events that may lead to losses for the Institution. When these events are identified based on operating losses, the social, environmental or climate scope is marked.

Compliance with laws and regulations

GRI 2-27

2-27 a) Report the total number of significant instances of non-compliance with laws and regulations during the reporting period, and a breakdown of this total by:

i. instances for which fines were incurred;

ii. instances for which non-monetary sanctions were incurred;

In 2024, no significant instances of non-compliance with laws and regulations were recorded.

2-27 b) Report the total number and the monetary value of fines for instances of noncompliance with laws and regulations that were paid during the reporting period, and a breakdown of this total by:

i. fines for instances of non-compliance with laws and regulations that occurred in the current reporting period;

ii. fines for instances of non-compliance with laws and regulations that occurred in previous reporting periods;

In 2024, no significant instances of non-compliance with laws and regulations were recorded. In previous reporting periods (2017-2023), four instances of non-compliance with laws and regulations were recorded and fines amounted to R$54 thousand.

2-27 c) Describe the significant instances of non-compliance;

Significant instances are those whose impact significantly affects the Institution’s results, image, or reputation.

2-27 d) Describe how it has determined significant instances of non-compliance.

Instances of non-compliance with social, environmental and climate-related regulations are identified based on Section VIII – Management of social, environmental and climate risks (articles 38-A, 38-B, 38-C) of the National Monetary Council’s Resolution 4,557/17.

Compliance with laws and regulations

GRI 2-27

In 2022, there were 1,085 significant instances of non-compliance with laws and regulations, of which only one incurred in fine (one instance of irregular waste disposal). 720 Municipal Tax Unit (UFM, in Portuguese) (R$3,554.06) repaid by the outsourced cleaning company (as set forth in the contract) and other non-monetary penalties. Out of the 1,084 administrative or judicial proceedings that did not incur in fines, 1,082 are social in scope: six are events related to accessibility, 20 to over-indebtedness, one to customer moral harassment, 1,055 are labor complaint events (according to CMN Resolution 4,943/21), one environmental event (disposal of recyclable waste in an organic waste container), one climate-related event (collection lawsuit to recover the amounts from the plaintiff’s property insurance policy, affected by a storm).

Additionally, Banrisul received 262 notifications in this reporting cycle, 45 of which were fines for instances of non-compliance with laws, and all of these were paid during previous reporting periods.

Compliance with laws and regulations

GRI 2-27

2-27 a) Report the total number of significant instances of non-compliance with laws and regulations during the reporting period, and a breakdown of this total by:

2-27 a) i) instances for which fines were incurred;

2-27 a) ii) instances for which non-monetary sanctions were incurred;

In 2025, no significant instances of non-compliance with laws and regulations were recorded.

2-27 b) Report the total number and the monetary value of fines for instances of noncompliance with laws and regulations that were paid during the reporting period, and a breakdown of this total by:

2-27 b) ii) fines for instances of non-compliance with laws and regulations that occurred in the current reporting period;

2-27 b) ii) fines for instances of non-compliance with laws and regulations that occurred in previous reporting periods;

Total number of fines for non-compliance with laws and regulations¹ | GRI 2-27 |

||||

|---|---|---|---|---|

2023 |

2024 |

2025 |

Δ 2025/2024 |

|

Number of cases |

362 |

483 |

429 |

-11.2% |

Monetary value |

195,216.9 |

148,366.8 |

255,431.4 |

72.2% |

¹ Despite the 11.2% decrease in the number of cases between 2024 and 2025, average fine amount increased, primarily due to enforcement actions by the Ministry of Labor, which resulted in fines imposed on branches with fewer apprentices than required by law (the Apprenticeship Law). Despite this variation, the total monetary value of the fines remains insignificant in the context of the Institution’s financial statements.

2-27 c) Describe the significant instances of non-compliance;

Significant cases are those whose impact materially affect the Institution’s results, image, or reputation.

2-27 d) Describe how it has determined significant instances of non-compliance.

Significant cases of non-compliance are determined based on impact assessment criteria that classify events as “high” or “severe” across the financial, reputational, regulatory, technological, third-party relations, social, environmental, and climate-related dimensions, as well as fines and legal actions. A case is considered significant when any of these dimensions reaches the aforementioned levels. The assessment uses quantitative (such as financial figures) and qualitative (such as media exposure and regulatory intervention) parameters to ensure consistency and comparability of the classifications. The criteria used are:

1. Financial Impact: Cases are considered significant when they result in financial impacts substantial enough to affect the institution’s financial performance or operational stability.

2. Reputational Impact: A case is considered significant when it results in significant negative exposure in the media, on social media, or among shareholders and investors, compromising the institution’s image.

3. Regulatory Impact: Events that require immediate response to regulatory authorities, or that result in direct intervention by regulatory bodies, are classified as significant.

4. Third-Party Impact: Incidents involving suppliers or service providers are considered significant when they substantially compromise the continuity, quality, or safety of essential processes.

5. Social, Environmental, and Climate Impact: Cases are classified as significant when they generate significant effects—or compromise fundamental processes—related to social, environmental, or climate aspects.

6. Technological Impact: Events that result in significant customer losses, operational instability, risks to business continuity, or damage to trust in technological systems are considered significant.7. Impact of Fines and Legal Actions: Fines or legal actions are classified as significant when they pose material risks to the Institution’s reputation, operational continuity, or financial security.

Conflicts of interest

GRI 2-15

2-15 a) Describe the processes for the highest governance body to ensure that conflicts of interest are prevented and mitigated.

Banrisul recognizes and manages conflicts of interest in all activities, including in relation to the Board of Directors, in accordance with the applicable legal rules, including Article 156 of Brazilian Corporate Law and Article 25 of the Bylaws.

In addition to the legal regulations, it has a Code of Ethics and Conduct and a Conflict of Interest Booklet for all those involved in the Banrisul Group, both of which are widely disseminated.

When it comes to credit transactions, compliance also includes the Related-Party Transaction Policy, which defines the conditions for these and other transactions to be carried out.

2-15 b) Report whether conflicts of interest are disclosed to stakeholders, including, at a minimum, conflicts of interest relating to:

2-15 b) i) cross-board membership;

The participation of management members in other positions in Banrisul Group companies is reported in item 7.6 of the 2023 Reference Form.

2-15 b) ii) cross-shareholding with suppliers and other stakeholders;

There are no shareholdings of suppliers or other stakeholders not listed in the 2023 Financial Statements, page 38.

2-15 b) iii) existence of controlling shareholders;

The only controlling shareholder is the State of Rio Grande do Sul.

2-15 b) iv) related parties, their relationships, transactions, and outstanding balances.

We refer to Note 29 to the 2023 Financial Statements. Note 29 – transactions with related parties:

(a) Transactions with related parties are disclosed in compliance with Technical Pronouncement CPC 05(R1) and CMN Resolution 4,818/20.Account balances relating to transactions between consolidated companies are eliminated in the consolidated financial statements and also take into account the absence of risk. With regard to transactions carried out with the State Government and entities fully or jointly controlled by it, we have opted for the partial exemption granted by CMN Resolution 4,818/20. In this case, only the most significant transactions are disclosed. We carry out banking transactions with related parties, including checking account deposits (non-interest-bearing), interest-bearing deposits, open market funding, loans and service contracts. These transactions are carried out at the usual average market amounts, terms and rates in force on the respective dates, on an arm’s length basis.

Conflicts of interest

GRI 2-15

2-15 a) Describe the processes for the highest governance body to ensure that conflicts of interest are prevented and mitigated;

We adopt strict practices to prevent and manage conflicts of interest, always complying with current laws, such as the Brazilian Corporate Law and the Company’s Bylaws. We also follow the guidelines established in our Code of Ethics and Conduct and our Handbook on Conflicts of Interest, which can be consulted by all parties involved. As for loan operations, control is reinforced by the Related-Party Transactions Policy, which sets out clear rules for conducting such transactions.

2-15 b) Report whether conflicts of interest are disclosed to stakeholders, including, at a minimum, conflicts of interest relating to:

2-15 b) i) cross-board membership;

Information on cross-membership among Banrisul Group companies is available on item 7.6 of the 2024 Reference Form (page 174).

2-15 b) ii) cross-shareholding with suppliers and other stakeholders;

There are no cross-shareholdings with suppliers or other stakeholders. Information available on the 2024 Financial Statements (page 35, BRGAAAP).

2-15 b) iii) existence of controlling shareholders;

The only controlling shareholder is the State of Rio Grande do Sul.

2-15 b) iv) related parties, their relationships, transactions, and outstanding balances.

Banking transactions with related parties, including interest bearing and non-interest-bearing deposits, open market funding, loans, and service agreements, are consistently carried out under prevailing market values, terms, and rates on their respective dates and under arm’s length principles. Related party transactions are disclosed in the Financial Statements, in compliance with regulations on the matter.

Conflicts of interest

GRI 2-15

Banrisul’s Board of Directors identifies and manages conflicts of interest based on, but not limited to, applicable legal standards provided for in Article 156 of the Brazilian Corporate Law and article 25 of its Bylaws. Furthermore, the Code of Ethics and Conduct is widely disseminated to management members, board members, employees, interns, members of the Banrisul Group, business partners, suppliers and service providers. In the event of a potential conflict of interest, members of the Board of Directors, the Audit Committee and the Ethics Committee must abstain from resolving on matters in which this conflict is identified. Another important document governing this topic is the Related-Party Transactions Policy that outlines the conditions credit transactions and other related-party transactions.

The item “SUBORDINATION, SERVICE OR CONTROL RELATIONSHIPS BETWEEN THE ISSUER’S MANAGEMENT AND ITS SUBSIDIARIES, AFFLIATES AND OTHERS” of the Company’s Reference Form informs the interest held by Banrisul management in management of other companies in the Banrisul Group. The only controlling shareholder is the State of Rio Grande do Sul.

Related-party transactions, as well as measures taken by Banrisul, can be found in Note 29, pages 118 and 119, to the 2022 Financial Statements, available here.

Conflicts of interest

GRI 2-15

2-15 a) Describe the processes for the highest governance body to ensure that conflicts of interest are prevented and mitigated.

We have adopted formal mechanisms to prevent, identify, and address conflicts of interest, ensuring that our corporate decisions are taken based on criteria of integrity, transparency, and alignment with institutional interests. These mechanisms are primarily set forth in our Code of Ethics and Conduct and in our internal governance policies, which guide the actions of management, employees, and other representatives of the Institution.

2-15 b) Report whether conflicts of interest are disclosed to stakeholders, including, at a minimum, conflicts of interest relating to:

2-15 b) i) cross-board membership;

Information on cross-shareholdings among Banrisul Group companies is available in item 7.6 of the 2025 Reference Form.

2-15 b) ii) cross-shareholding with suppliers and other stakeholders;

There are no cross-shareholdings with suppliers or other unrelated parties.

2-15 b) iii) existence of controlling shareholders;

The sole controlling shareholder is the State.

2-15 b) iv) related parties, their relationships, transactions, and outstanding balances.

Related parties, their relationships, transactions, and outstanding balances are disclosed in the 2025 IFRS Financial Statements, in accordance with IAS 24 and CMN Resolution No.4,818/20, covering transactions conducted on an arm’s-length basis, with the elimination of intercompany balances within the Group in the consolidated financial statements and the disclosure of material transactions with the State of Rio Grande do Sul and its entities.

Delegation of responsibility for managing impacts

GRI 2-13

2-13) Describe how the highest governance body delegates responsibility for managing the organization’s impacts on the economy, environment, and people, including:

2-13 a) i) whether it has appointed any senior executives with responsibility for the management of impacts;

Executive risk management is led by the Executive Superintendent of Corporate Risks.

2-13 a) ii) whether it has delegated responsibility for the management of impacts to other employees;

Executive risk management is led by the Executive Superintendent of Corporate Risks, who reports directly to the CRO. This executive coordinates the unit responsible for conducting the integrated management of risks pertaining to credit, market, IRRBB (interest rate risk in the banking book), liquidity, operational, social, environmental and climate, covering all companies in the Conglomerate, including subsidiaries.

2-13 b) Describe the process and frequency for senior executives or other employees to report back to the highest governance body on the management of the organization’s impacts on the economy, environment, and people.

On a quarterly basis, the Board of Directors addresses the topic of social, environmental, and climate risks and responsibility, and impacts related thereto, together with the Social, Environmental, and Climate Responsibility Committee.

Delegation of responsibility for managing impacts

GRI 2-13

2-13 a) Describe how the highest governance body delegates responsibility for managing the organization’s impacts on the economy, environment, and people, including:

a) i) whether it has appointed any senior executives with responsibility for the management of impacts;

The implementation of the Social, Environmental, and Climate Responsibility Policy (PRSAC) is led by the Chief Risk Officer (CRO).

2-13 a) ii) whether it has delegated responsibility for the management of impacts to other employees;

The Executive Superintendent of Corporate Risks is formally designated as responsible for managing social, environmental, and climate risks and impacts.

2-13 b) Describe the process and frequency for senior executives or other employees to report back to the highest governance body on the management of the organization’s impacts on the economy, environment, and people.

SAC risk management is exercised through structured reporting, including the Social, Environmental, and Climate Risk and Responsibility Report submitted to the Board. This matter is also reported monthly to the Social, Environmental, and Climate Responsibility Committee and quarterly to the Board of Directors.

Delegation of responsibility for managing impacts

GRI 2-13

The Control and Risk Executive Office is responsible for managing the Institutions’ corporate risks.

As regards Integrated Capital and Corporate Risk Management, the Chief Risk Officer (CRO) is responsible for the Corporate Risk Management Department and his/her duties include ensuring that the risk process monitors, controls, evaluates and plans capital need and goals and identifies, measures, monitors, reports, controls and mitigates credit, market, IRRBB, liquidity, operational, social, environmental and climate risks associated with the Prudential Conglomerate, communicating said risks to the Risk Committee, the CEO, the Board of Directors and regulatory agencies.

The Corporate Risk Executive Superintendent reports to the CRO on the Institution’s risk management. At least every year, risk management reports are submitted to the Board of Directors for consideration.

Delegation of responsibility for managing impacts

GRI 2-13

2-13 a) Describe how the highest governance body delegates responsibility for managing the organization’s impacts on the economy, environment, and people, including:

2-13 a) i) whether it has appointed any senior executives with responsibility for the management of impacts;

The Board of Directors is responsible for steering the Bank’s business, guidelines and institutional goals. It is advised by the Audit, Risk, Eligibility and Compensation, and Social, Environmental and Climate Responsibility Committees, all of which operate on a permanent basis.

The Corporate Risk Executive Superintendent reports to the Chief Risk Officer (CRO) on the Institution’s risk management. The executive is responsible for the Corporate Risk Unit and for coordinating capital management and credit, market, IRRBB, liquidity, operational, social, environmental and climate risks, covering all the institutions in the Prudential Conglomerate. It also considers the possible impacts of risks associated with other companies controlled by Conglomerate companies and other significant risks identified.

In 2023, the Risk Office incorporated sustainability into the Social, Environmental and Climate Risk Department, with the intention of reinforcing the importance of sustainability and promoting integrated action on related risks and opportunities. Thus, the management of the Social, Environmental and Climate Responsibility Policy is aligned with the risk guidelines, integrating processes and directing the focus of its risk and responsibility initiatives.

2-13 a) ii) whether it has delegated responsibility for the management of impacts to other employees.

The corporate risk executive superintendent reports to the Chief Risk Office (CRO) on the Institution’s risk management.

2-13 b) Describe the process and frequency for senior executives or other employees to report back to the highest governance body on the management of the organization’s impacts on the economy, environment, and people.

The Institution has developed a series of indicators and flags to monitor its risk appetite, which are periodically monitored and reported to Senior Management by means of reports and a dashboard. The risk matrix is updated dynamically, with attention to the risks with the greatest exposure. Processes are monitored according to the frequency and impact of their respective risks. The Risk Appetite Statement (RAS), documented for Banrisul’s Prudential Conglomerate, is reviewed annually with the support of the Risk Committee, the Board of Executive Officers and the Chief Risk Officer (CRO).

Embedding policy commitments

GRI 2-24

The credit policies definitions are available in internal regulations and are also parameterized in the “Customer Registration”, “Negative Incidents” and “Risk Calculation” systems. The Bank currently checks with external agencies whether the customer, either an individual or a company, has been listed as an “Employer that uses Forced Labor” or as causing “Environmental Damage” (conviction for environmental damage in actions filed by Brazil’s environmental protection agency (IBAMA, in Portuguese)).

Customers identified as “Employer of Forced Labor” are prevented from contracting any type of credit operations. We also monitor customers who already have a relationship with us and who may be included in those lists, taking specific actions to discontinue the business relationship.

Embedding policy commitments

GRI 2-24

2-24 a) Describe how it embeds each of its policy commitments for responsible business conduct throughout its activities and business relationships, including:

In its relationship with the various sectors of society, Banrisul acts based on principles of institutional conduct designed to value people and respect human rights. These principles are described in a series of institutional policies, approved by the Board of Directors, which determine the conduct expected of employees, contractors and suppliers.

2-24 a) i) how it allocates responsibility to implement the commitments across different levels within the organization;

The Ethics Committee, which reports to the Chief Executive Officer, is the body responsible for implementing, disseminating, training, reviewing and updating Banrisul’s Code of Ethics and Conduct in order to ensure its efficacy and effectiveness, in addition to analyzing and judging the issues submitted to it, recommending correction of conduct or disciplinary sanctions. The Committee has autonomy and operates independently. In the event of a conflict of interest, the Board of Executive Officers takes the final decision.

2-24 a) ii) how it integrates the commitments into organizational strategies, operational policies, and operational procedures;

Banrisul has an Ethics Committee responsible for implementing, disseminating, training, reviewing and updating Banrisul’s Code of Ethics and Conduct in order to ensure its efficacy and effectiveness, in addition to analyzing and judging the issues submitted to it, recommending correction of conduct or disciplinary sanctions. Therefore, it is incumbent upon the Ethics Committee to carry out this integration process, through policies and training.

Moreover, we had the Privacy and Data Protection Governance Program, which was responsible for integrating data protection commitments.

2-24 a) iii) how it implements its commitments with and through its business relationships;

In its relationship with the various sectors of society, Banrisul acts based on principles of institutional conduct designed to value people and respect human rights. These principles are described in a series of institutional policies, approved by the Board of Directors, which determine the conduct expected of employees, contractors and suppliers. These policies are communicated by means of an Administrative Instruction.

2-24 a) iv) training that the organization provides on implementing the commitments.

All employees receive training on the Code of Ethics and Conduct and the Anti-Corruption Code.

As regards data protection, the Data Privacy and Protection Governance Program was set up this year, comprising several fronts, including:

- Mapping of all activities involving personal data processing, identifying the data life cycle, from collection to deletion, and the appropriate legal framework;

- Creation of a customer service channel for holders of personal data, ensuring the full exercise of all the rights set out in the Brazilian General Data Protection Law (LGPD, in Portuguese);

- Formalization in a standard of a flow of adjustments of contracts with third parties to comply with the LGPD, including the definition of a methodology to help identify the Processor x Controller x Joint Controllers and define the flow for indicating LGPD clauses for business and administrative contracts;

- Implementation of the Privacy by Design and Privacy by Default methodologies in order to ensure the privacy and protection of personal data in the design of new products and services;

- Creation of specific guidelines for handling or responding to security incidents involving personal data, considering the requirements imposed by the LGPD in order to complement Banrisul’s existing Information and Cyber Security Policy; and

- Development of internal training for all the staff on the main points addressed by the Law and their impacts on the workplace, as well as creation of a website featuring content that helps disseminate a culture of data privacy and protection in the Institution.

Embedding policy commitments

GRI 2-24

2-24 a) Describe how it embeds each of its policy commitments for responsible business conduct throughout its activities and business relationships, including:

2-24 a) i) How it allocates responsibility to implement the commitments across different levels within the organization;

We operate through Banrisul’s Social, Environmental and Climate Responsibility Policy (PRASC, in Portuguese), which sets forth the assumptions, goals, principles and guidelines that drive the social, environmental and climate responsibility actions of the companies belonging to the Banrisul Prudential Conglomerate and how it operates with entities controlled by these companies or in which they own an equity stake. We established several actions under the social, environmental and climate aspects to affirm the Bank’s commitment to the most diverse sustainability topics.

Sustainability is a cross-cutting topic in Banrisul’s Strategic Plan and focuses on generating positive impacts, mitigating risks, developing sustainable solutions, and supporting its customers’ transition to a more inclusive, resilient, and low-carbon economy.

We also made other relevant commitments, such as the Financial Education Policy, which promotes inclusion and sustainable development through financial empowerment of the population, focused on microentrepreneurs and vulnerable regions.

2-24 a) ii) how it integrates the commitments into organizational strategies, operational policies, and operational procedures;

Banrisul’s Ethics Committee is responsible for implementing, disseminating, training, reviewing and updating the Code of Ethics and Conduct in order to ensure its efficacy and effectiveness, in addition to analyzing and deciding on the matters submitted to it, recommending correction of conduct or disciplinary sanctions.

The Risk Department is responsible for implementing the Social, Environmental, and Climate Responsibility Policy (PRSAC, in Portuguese), as well as the Social, Environmental, and Climate Risk Management Policy. The department carries out and oversees actions related to social, environmental, and climate issues, including impact management.

While our integrated impact management process is still being consolidated, the Bank has already established internal mitigation and oversight processes, including works by the Internal Audit, which contribute to the enabling effective actions.

The Privacy and Data Protection Governance Program was responsible for integrating data protection commitments.

2-24 a) iii) how it implements its commitments with and through its business relationships;

The principles of institutional conduct are outlined in a series of corporate policies, approved by the Board of Directors, which establish the expected behavior of employees, service providers, and suppliers. These policies are communicated by means of an Administrative Instruction.

2-24 a) iv) training that the organization provides on implementing the commitments.

All employees receive training on the Code of Ethics and Conduct and the Anti-Corruption Code.

As regards data protection, the Data Privacy and Protection Governance Program was set up this year, comprising several fronts, including the development of internal training sessions for all employees.

As regards sustainability, we promote the dissemination of sustainable practices through our communication channels with stakeholders and offer distance learning courses and themed events to our internal audience.

Embedding policy commitments

GRI 2-24

2-24 a) Describe how it embeds each of its policy commitments for responsible business conduct throughout its activities and business relationships, including:

2-24 a) i) how it allocates responsibility to implement the commitments across different levels within the organization;

The Executive Board is responsible for executing the strategies and guidelines approved by the Board of Directors, ensuring the efficient management of resources, implementing corporate policies, and conducting operations in accordance with regulatory standards and established strategic guidelines.

The implementation of the Code of Ethics and Conduct is monitored by the Ethics Committee.

2-24 a) ii) how it integrates the commitments into organizational strategies, operational policies, and operational procedures;

This topic is managed through the Integrity Program, which brings together policies, procedures, and control mechanisms aimed at preventing, identifying, and addressing conduct inconsistent with institutional principles.

2-24 a) iii) how it implements its commitments with and through its business relationships;

Business relationships with partners and suppliers are formalized through contracting and monitoring processes that take into account technical, legal, and compliance criteria.

Our contracting and evaluation processes are designed to ensure compliance with legal requirements, labor practices, and respect for human rights, thereby helping to reduce social and environmental risks across our supply chain.

2-24 a) iv) training that the organization provides on implementing the commitments.

As part of our efforts to strengthen our culture of integrity, we provide mandatory training on ethics and prevention of corruption for all employees. In 2025, we also held workshops on prevention of harassment for senior management and middle management, with plans to expand this initiative in 2026.

Employees

GRI 2-7

Employees, by gender¹ ²

2020 |

2021 |

2022 |

|||||||

|---|---|---|---|---|---|---|---|---|---|

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

|

Permanent and full-time employees |

5,129 |

4,151 |

9,280 |

4,946 |

4,056 |

9,002 |

4,729 |

3,929 |

8,658 |

¹Banrisul does not have temporary, non-guaranteed hours and part-time employees.

²All permanent employees are full-time employees.

Employees, by region

Region¹ |

2020 |

2021 |

2022 |

|---|---|---|---|

Midwest |

9 |

7 |

8 |

South |

9,214 |

8,939 |

8,600 |

Southeast |

57 |

56 |

50 |

Total |

9,280 |

9,002 |

8,658 |

¹Banrisul does not have employees in the North and Northeast regions.

Data were gathered from a proprietary system, considering total employees for the reference period.

Employees

GRI 2-7

2-7 a) Report the total number of employees, and a breakdown of this total by gender and by region.

2-7 b) Report the total number of:

2-7 b) i) permanent employees, and a breakdown by gender and by region;

2-7 b) ii) temporary employees, and a breakdown by gender and by region;

2-7 b) iii) non-guaranteed hours employees, and a breakdown by gender and by region;

2-7 b) iv) full-time employees, and a breakdown by gender and by region;

2-7 b) v) part-time employees, and a breakdown by gender and by region.

Employee information, by gender¹ | GRI 2-7 |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Type of employment contract |

2023 |

2024 |

2025 |

Δ 2025/2024 |

||||||||

Men |

Women |

Total |

Men |

Women |

Total |

Man |

Women |

Total |

Man |

Women |

Total |

|

Permanent, full-time employees |

5,192 |

3,897 |

9,089 |

5,458 |

4,004 |

9,462 |

5,306 |

3,922 |

9,228 |

-2,8% |

-2,0% |

-2,5% |

¹ There are no temporary, non-guaranteed-hour, or part-time employees.

Employee information, by region¹ | GRI 2-7 |

|||||

|---|---|---|---|---|---|

Employment type |

Region |

2023 |

2024 |

2025 |

Δ 2025/2024 |

Full-time employees |

Midwest |

7 |

7 |

7 |

0.0% |

South |

9,032 |

9,419 |

9,177 |

-2.6% |

|

Southeast |

50 |

36 |

44 |

22.2% |

|

Total |

9,089 |

9,462 |

9,228 |

-2.5% |

|

¹ There are no temporary, non-guaranteed-hour, or part-time employees.

2-7 c) Describe the methodologies and assumptions used to compile the data, including whether the numbers are reported:

2-7 c) i) in head count, full-time equivalent (FTE), or using another methodology;

2-7 c) ii) at the end of the reporting period, as an average across the reporting period, or using another methodology.

The data was generated using reports from the company’s own HR systems, based on year-end totals.

2-7 d) Report contextual information necessary to understand the data reported under 2-7 a) and 2-7 b).

All permanent employees reported are considered full-time.

2-7 e) Describe significant fluctuations in the number of employees during the reporting period and between reporting periods.

There were no significant changes.

Employees

GRI 2-7

2-7 a) Report the total number of employees, and a breakdown of this total by gender and by region;

2-7 b) Report the total number of:

i. permanent employees, and a breakdown by gender and by region;

ii. temporary employees, and a breakdown by gender and by region;

iii. non-guaranteed hours employees, and a breakdown by gender and by region;

iv. full-time employees, and a breakdown by gender and by region;

v. part-time employees, and a breakdown by gender and by region;

Employees, and a breakdown by employment contract type and by gender¹ |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

2022 |

2023 |

2024 |

Δ 2024/2023 |

|||||||||

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

|

Permanent and full-time employees |

4,729 |

3,929 |

8,658 |

5,192 |

3,897 |

9,089 |

5,458 |

4,004 |

9,462 |

5.1% |

2.7% |

4.1% |

Total |

4,729 |

3,929 |

8,658 |

5,192 |

3,897 |

9,089 |

5,458 |

4,004 |

9,462 |

5.1% |

2.7% |

4.1% |

¹ There are no temporary, non-guaranteed hours and part-time employees.

Employees, and a breakdown by employment contract type and by region¹ |

|||||

|---|---|---|---|---|---|

2022 |

2023 |

2024 |

Δ 2024/2023 |

||

Permanent and full-time employees |

Midwest |

8 |

7 |

7 |

0.0% |

South |

8,600 |

9,032 |

9,419 |

4.3% |

|

Southeast |

50 |

50 |

36 |

-28.0% |

|

Total |

8,658 |

9,089 |

9,462 |

4.1% |

|

Total |

Midwest |

8 |

7 |

7 |

0.0% |

South |

8,600 |

9,032 |

9,419 |

4.3% |

|

Southeast |

50 |

50 |

36 |

-28.0% |

|

Total |

8,658 |

9,089 |

9,462 |

4.1% |

|

¹ There are no temporary, non-guaranteed hours and part-time employees. There are no employees in the North and Northeast regions.

2-7 c) Describe the methodologies and assumptions used to compile the data, including whether the numbers are reported:

i. in head count, full-time equivalent (FTE), or using another methodology;

ii. at the end of the reporting period, as an average across the reporting period, or using another methodology;

Data was generated based reports from HR’s own systems, considering the totals at the end of the year.

2-7 d) Report contextual information necessary to understand the data reported under 2-7-a and 2-7-b;

All permanent employees reported are full-time employees.

2-7 e) Describe significant fluctuations in the number of employees during the reporting period and between reporting periods.

In 2024, we hired employees through the IT II and clerk civil service exams.

Employees

GRI 2-7

2-7 a) Report the total number of employees, and a breakdown of this total by gender and by region.

2-7 b) Report the total number of:

2-7 b) i) permanent employees, and a breakdown by gender and by region;

2-7 b) ii) temporary employees, and a breakdown by gender and by region;

2-7 b) iii) non-guaranteed hours employees, and a breakdown by gender and by region;

2-7 b) iv) full-time employees, and a breakdown by gender and by region;

2-7 b) v) part-time employees, and a breakdown by gender and by region.

2021 |

2022 |

2023 |

|||||||

|---|---|---|---|---|---|---|---|---|---|

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

Masculine |

Feminine |

Total |

|

Permanent and full-time employees |

4,946 |

4,056 |

9,002 |

4,729 |

3,929 |

8,658 |

5,192 |

3,897 |

9,089 |

¹There are no temporary, non-guaranteed hours and part-time employees.

2021 |

2022 |

2023 |

||

|---|---|---|---|---|

Permanent and full-time employees |

Midwest |

7 |

8 |

7 |

South |

8,939 |

8,600 |

9,032 |

|

Southeast |

56 |

50 |

50 |

|

Total |

9,002 |

8,658 |

9,089 |

¹There are no temporary, non-guaranteed hours and part-time employees. There are no employees in the North and Northeast regions.

2-7 c) Describe the methodologies and assumptions used to compile the data, including whether the numbers are reported:

2-7 c) i) in head count, full-time equivalent (FTE), or using another methodology;

2-7 c) ii) at the end of the reporting period, as an average across the reporting period, or using another methodology.

Data was generated based reports from HR’s own systems, considering the totals at the end of the year.

2-7 d) Report contextual information necessary to understand the data reported under 2-7-a and 2-7-b.

All permanent employees reported are full-time employees.

2-7 e) Describe significant fluctuations in the number of employees during the reporting period and between reporting periods.

There was a 5.0% increase in employees between 2022 and 2023. To strengthen the team and bring new talent to the Institution, 244 new employees joined the IT departments and 898 employees joined the branch network in 2023.

Entities included in the organization’s sustainability report

GRI 2-2

2-2 a) List all its entities included in its sustainability reporting.

The conglomerate comprises Banco do Estado do Rio Grande do Sul and the following subsidiaries and affiliates: Banrisul Armazéns Gerais S.A; Banrisul S.A. Corretora de Valores Mobiliários e Câmbio; Banrisul S.A. Administradora de Consórcios; Banrisul Soluções em Pagamentos S.A.; and Banrisul Seguridade Participações S.A., all of which are included in the report and the financial statements.

2-2 b) If the organization has audited consolidated financial statements or financialinformation filed on public record, specify the differences between the list of entitiesincluded in its financial reporting and the list included in its sustainability reporting.

The Sustainability Report presents Banrisul’s consolidated information; other entities are not included.

2-2 c) If the organization consists of multiple entities, explain the approach used forconsolidating the information, including:

The approach used in the Sustainability Report concerns the company’s business or service, not necessarily its shareholding structure.

2-2 c) i) whether the approach involves adjustments to information for minority interests;

It does not.

2-2 c) ii) how the approach takes into account mergers, acquisitions, and disposal ofentities or parts of entities;

There were no mergers, acquisitions or disposals.

2-2 c) iii) whether and how the approach differs across the disclosures in this Standard and across material topics.

It does not.

Entities included in the organization’s sustainability reporting

GRI 2-2

2-2 a) List all its entities included in its sustainability reporting.

With regard to the organizational scope, this report includes consolidated information about Banrisul – Banco do Estado do Rio Grande do Sul S.A. and the group comprising the following subsidiaries and affiliates: Banrisul Armazéns Gerais S.A.; Banrisul S.A. Corretora de Valores Mobiliários e Câmbio; Banrisul S.A. Administradora de Consórcios; Banrisul Soluções em Pagamentos S.A.; and Banrisul Seguridade Participações S.A.

2-2 b) If the organization has audited consolidated financial statements or financial information filed on public record, specify the differences between the list of entities included in its financial reporting and the list included in its sustainability reporting.

The Sustainability Report includes consolidated information about Banrisul and the group, all of which is included in the report as well as in the financial statements.

2-2 c) If the organization consists of multiple entities, explain the approach used for consolidating the information, including:

2-2 c) i) whether the approach involves adjustments to information for minority interests;

The approach used does not involve adjustments to information related to minority interests.

2-2 c) ii) how the approach takes into account mergers, acquisitions, and disposal of entities or parts of entities;

There were no mergers, divestments, or acquisitions.

2-2 c) iii) whether and how the approach differs across the disclosures in this Standard and across material topics.

The approach used is consistent throughout this Standard and the material topics.

Entities included in the organization’s sustainability reporting

GRI 2-2

The consolidated financial statements include the operations of Banrisul, its offices abroad, its subsidiaries (Banrisul Armazéns Gerais S.A., Banrisul S.A. Corretora de Valores Mobiliários e Câmbio, Banrisul S.A. Administradora de Consórcios, Banrisul Soluções em Pagamentos S.A., Banrisul Seguridade Participações S.A.) and investment fund quotas in which Banrisul substantially takes or incurs in risks and benefits. We explain the Banrisul Group in detail, which comprises six subsidiaries and four affiliated companies.

Entities included in the organization’s sustainability reporting

GRI 2-2

2-2 a) List all its entities included in its sustainability reporting;

The report integrates data from Banco do Estado do Rio Grande do Sul (operations in Brazil and, in fiscal year 2023, foreign subsidiaries) and controlled companies: Banrisul Armazéns Gerais S.A., Banrisul S.A. Corretora de Valores Mobiliários e Câmbio, Banrisul S.A. Administradora de Consórcios, Banrisul Soluções em Pagamentos S.A., and Banrisul Seguridade Participações S.A.

2-2 b) If the organization has audited consolidated financial statements or financial information filed on public record, specify the differences between the list of entities included in its financial reporting and the list included in its sustainability reporting;

The Sustainability Report presents Banrisul’s consolidated information; other entities are not included.

2-2 c) If the organization consists of multiple entities, explain the approach used for consolidating the information, including:

2-2 c) i) whether the approach involves adjustments to information for minority interests;

The approach used in the Sustainability Report concerns the Company’s businesses and services, not necessarily its shareholding structure.

2-2 c) ii) how the approach takes into account mergers, acquisitions, and disposal of entities or parts of entities;

There were no mergers, acquisitions or disposals in the reporting period.

2-2 c) iii) whether and how the approach differs across the disclosures in this Standard and across material topics.

It does not.

Evaluation of the performance of the highest governance body

GRI 2-18

Performance evaluation is an essential step to assess effectiveness, contributing to enhance the Organization’s governance. The Board of Directors carries out an annual formal evaluation of the Executive Board and its Chair performance, as well as of its own performance, a process that include self-evaluation questions. The annual evaluation is carried out according to procedures previously defined by the Board of Directors and is anonymous and individual.

All answers to the evaluation questionnaires are compiled into a report, which is sent to the Eligibility and Compensation Committee for prior analysis and then presented to the Board of Directors for consideration. The body itself suggests improvements in carrying out their duties.

Evaluation of the performance of the highest governance body

GRI 2-18

2-18 a) Describe the processes for evaluating the performance of the highest governance body in overseeing the management of the organization’s impacts on the economy, environment, and people.

The Board of Directors is subject to a formal performance evaluation with the aim of gauging effectiveness and improving Banrisul’s governance — an evaluation similar to the one applied annually to the Board of Executive Officers and the Chief Executive Officer. The evaluation process complies with Law 13,303/16 and State Decree 54,110/18, covering self-evaluation and comparison of the results obtained with the targets set, among others.

2-18 b) Report whether the evaluations are independent or not, and the frequency of the evaluations.

Performance appraisals are carried out annually, anonymously, individually and non-independently.

2-18 c) Describe actions taken in response to the evaluations, including changes to the composition of the highest governance body and organizational practices.

All answers to the evaluation questionnaires are compiled into a report, which is sent to the Eligibility and Compensation Committee for prior analysis and then presented to the Board of Directors for consideration. The body suggests improvements in carrying out their duties.

Evaluation of the performance of the highest governance body

GRI 2-18